Introduction

Space Robotics Statistics: Space robotics has kind of turned into one of the more transformative technologies shaping the modern space economy in 2026. Robotic systems are now becoming essential for satellite servicing, space station upkeep, lunar reconnaissance, autonomous navigation, debris clearing, in-orbit manufacturing, and even those upcoming Mars missions that everyone keeps talking about. Government agencies like NASA, the European Space Agency, Japan Aerospace Exploration Agency, and the Canadian Space Agency, plus commercial players, are putting billions of dollars into robotic technologies. This is helping lower mission costs, while also boosting operational safety, which is kind of a big deal.

At the same time, advances in artificial intelligence, autonomous handling, machine vision, and remote control operations have pushed the adoption of robotic systems across the whole space sector. And as lunar infrastructure programs get real, and commercial satellite constellations keep expanding, space robotics is showing up as one of the fastest-growing slices of the global space industry.

Editor’s Choice

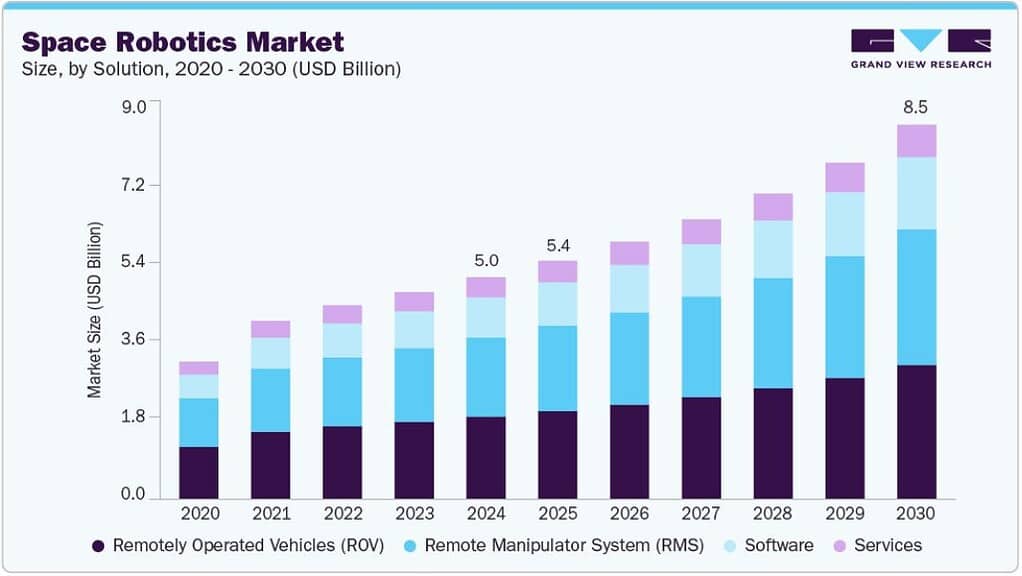

- The global space robotics market is expected to climb from USD 5.04 billion in 2024 to USD 8.50 billion by 2030, which really points to strong demand for automation in space.

- A healthy 9.5% CAGR through 2030 suggests the sector is moving from prototype experiments to operational infrastructure, not just demos anymore.

- North America held 40.39% of global revenue in 2024, basically confirming its lead role in robotic space technologies.

- Remotely operated vehicles, or ROVs, made up 37.77% of market revenue, which means they remain the biggest technology slice.

- Government agencies stayed as the main customers, contributing 70.13% of total market revenue in 2024, so yeah, public spending still dominates.

- Space robotics drew around USD 3 billion in public and private funding during 2025, which was seen as a sign of serious investor confidence.

- NASA’s OSAM-1 program went past USD 2 billion in development costs, and it kind of had three robotic arms. One of them was a 16-foot robotic manipulator.

- The Active Debris Removal (ADR) market is expected to grow from USD 452 million in 2024 up to USD 2.52 billion by 2032, and yes, it’s doing that at a very strong 29.9% CAGR, which is, honestly, impressive.

- Right now, there are over 36,000 trackable debris objects circling Earth, and that creates a big commercial opening for robotic cleanup services.

- For lunar logistics, the requirements are projected to rise from 800 kilograms to 15,000 kilograms per traverse, so like a nearly 19-times increase.

Global Space Robotics Market

(Source: grandviewresearch.com)

- In a broader sense, the global space robotics market is moving into a strong growth stage because automation is becoming more important for current space missions.

- Market stats show the industry was worth USD 5.04 billion in 2024, and it’s forecast to reach USD 8.50 billion by 2030. That’s growing with a compound annual growth rate (CAGR) of 9.5% from 2025 to 2030.

- Regionally, North America held the biggest share, with 40.39% of revenue in 2024, so it became the top contributor to global space robotics spending.

- The United States, in particular, made up most of North America’s revenue, which just reinforces its position as the leading place for robotic space technologies and advanced mission buildouts.

- On the technology side, Remotely Operated Vehicles (ROVs) came out as the biggest slice, grabbing 37.77% of total market revenue in 2024.

- By application, the Near Space segment kind of held the largest share at 46.13% in 2024, showing that a big chunk of robotic activity is kind of centered around orbital and near-Earth work.

- Government organizations stayed the main driver, bringing in 70.13% of total market revenue, which in turn underscores how national space agencies and public-sector initiatives really keep robotic innovation funded.

- The above numbers point to rising investments in robotic systems focused on satellite servicing, orbital tasks, and deep-space exploration.

Space Robotics Investment Boom

- The space robotics sector is moving quickly from a research-heavy landscape to a commercial growth industry.

- In 2025, space robotics companies pulled in roughly USD 3 billion in combined private and public funding, which signals solid investor trust in autonomous space operations.

- A handful of major firms then secured sizable capital: Astrobotic with more than USD 100 million in cumulative funding, GITAI over USD 70 million, and Orbit Fab with USD 60 million, aimed at maturing in-space refuelling technologies.

- Unlike many emerging technology startups, space robotics firms get this big advantage from government-backed income streams during the whole development period.

- Astrobotic has built up a NASA contract portfolio, above USD 600 million, while the more established names like Maxar keep landing multi-billion dollar government awards.

- In practice, these funding setups provide financial stability and, yes, they also lower commercialization risks while the new robotic technologies keep maturing.

- At the same time, technology development is leaning more and more toward autonomous operations. Communication delays still drive a lot of the pain here, with round-trip latency landing around 2.6 seconds between Earth and the Moon, and for Mars missions, it can stretch from 4 to 24 minutes.

- Market projections remain, honestly, pretty optimistic. Industry analysts think the global space robotics market might climb to USD 32 to USD 40 billion by 2032, powered by a strong 19% compound annual growth rate (CAGR).

- The growth story is being linked to wider lunar exploration efforts, satellite servicing networks, commercial space station maintenance, autonomous assembly systems, and then in-space manufacturing operations too.

- With USD 2.1 billion in annual venture investment, plus hundreds of millions of dollars in government contracts, and a projected USD 32 to USD 40 billion market opening by 2032, the sector looks like it’s shifting from experimental capability into essential space infrastructure.

- The next ten years will probably be defined by companies that can scale autonomous robotic services into dependable, repeatable commercial businesses that actually stick around.

Space Robotics OSAM-1 and The Rise Of Autonomous Orbital Infrastructure

- NASA’s OSAM-1 mission seemed like one of the most daring robotic tech tryouts ever pushed in Earth orbit.

- One standout part was the robotic architecture, kind of right in the center of the design. OSAM-1 was built to work with three robotic arms altogether.

- Two dexterous robotic arms were there for servicing work, while the third robotic arm was tied to the Space Infrastructure Dexterous Robot, also known as SPIDER. So, in practice, OSAM-1 counts as one of NASA’s most robotics-heavy craft for true autonomous in-orbit operations.

- The SPIDER robotic setup included a 16-foot, 5-meter arm that could handle tricky assembly actions in space.

- Through robotic manipulation, SPIDER was meant to put together seven different structural pieces into a working 9-foot, 3-meter communications antenna.

- In other words, the mission aimed to demonstrate robotic construction of big space structures, with no astronaut involvement at all, or at least none expected.

- A further milestone leaned into orbital manufacturing. SPIDER was also intended to manufacture a 32-foot, 10-meter lightweight composite beam directly in orbit.

- Despite its technological significance, OSAM-1 ran into big programmatic trouble in a kind of messy way. Congress put in USD 227 million for FY2024, while NASA was still assessing a tweaked mission structure aimed at a 2026 launch.

- Industry reporting also suggests that the overall program costs topped USD 2 billion, which makes OSAM-1 one of the priciest space robotics demonstration efforts that anyone has really tried.

- OSAM-1 was less about one discrete flight and more about testing what comes next for space robotics. It used three robotic arms, a 16-foot robotic manipulator, which supported assembly of a 9-foot antenna, then a 32-foot beam manufacturing step, plus integration involving five advanced robotic technologies.

- Together, the mission basically showed the magnitude of automation that future orbital infrastructure will need.

Active Debris Removal (ADR) and End-Of-Life De-Orbiting

- Active Debris Removal (ADR) and end-of-life de-orbiting have gone from experimental notions to one of the more promising commercial lanes in the space economy.

- The global ADR market was valued at about USUSD 452 million during 2024, and it’s expected to climb to roughly USUSD 614 million in 2025, then continue pushing up to close to USUSD 2.52 billion by 2032.

- An impressive 29.9% compound annual growth rate (CAGR), so ADR ends up looking like one of the quicker-expanding pockets inside the bigger space industry, at least from the numbers side.

- Some estimates say the global sector for space debris monitoring and removal sits near USD 1.05 billion in 2024, with projections pointing toward around USD 2.05 billion by 2033.

- In other words, orbital sustainability is shifting from “nice-to-have” into something more like a mainstream commercial chance.

- The European Space Agency (ESA) notes that more than 36,000 debris pieces that can be tracked are currently circling Earth, while hundreds of millions of tinier fragments stay untracked, and they’re still there doing their quiet damage.

- The danger those objects bring to a space-enabled economy, reported at over USD 300 billion per year, adds pressure on regulators and operators to take responsible disposal practices more seriously, not just as policy words.

- On top of that, commercial demonstration work is moving along fairly fast. ESA’s ClearSpace-1 mission is aiming to capture and de-orbit the 95-kilogram Proba-1 satellite, and that’s meant to show the practicality of robotic debris-removal services.

- Astroscale’s ADRAS-J mission made a successful approach to a spent 3-ton H-2A rocket stage, measuring roughly 11 meters long and 4 meters across, and it managed to maneuver to within about 15 meters of the object.

- The bigger satellite servicing market is projected to rise from something like USD 3.1 billion in 2026 to roughly USD 6.1 billion by 2033, with the backup reason coming from more demand for life-extension services, orbital upkeep, refuelling, plus de-orbiting capabilities.

- The above figures imply that ADR and end-of-life disposal are becoming a key pillar for the coming space economy.

Lunar Surface Mobility and Regolith Operations

- Lunar surface robotics has become one of the most strategically important segments within the global space economy in 2026.

- Instead of classic space robotics that mainly targets spacecraft in orbit, these lunar robots are now being built to move cargo, check out resources, assemble infrastructure, and help with long-duration human presence on the Moon.

- The level of investment hints at how much these systems matter inside NASA’s Artemis program, as well as for allied international lunar efforts.

- Present lunar mobility systems can move only about 800 kilograms per traverse, while upcoming Artemis logistics concepts expect to shift up to 15,000 kilograms of cargo between landing areas and working zones. That almost 19-times increase in transport demands is already pushing substantial government funding toward advanced rover design and construction-robot technologies.

- NASA’s planned Lunar Terrain Vehicle (LTV) kind of shows how rough the performance targets really are for the next wave of lunar robotics.

- With Artemis, the specs say the LTV must haul 800 kilograms of cargo, move as much as 20 kilometers before it needs any recharging, run for 8 hours during a 24-hour window, and keep working on slopes of up to ±20 degrees.

- In other words, these numbers indicate the shift from more exploratory rover types into industrial-grade mobility systems that are less “one-off” and more reliable.

- Astrobotic’s MoonRanger rover really points at the move toward lightweight autonomous fieldwork. It comes in around 13-18 kilograms, and it’s built to function for one lunar day about 14 Earth days while mapping terrain on its own and looking for hydrogen-bearing resources.

- The design also includes about 16-centimeter ground clearance, and it can climb slopes up to 15 degrees, so even for a small robot platform, the engineering still has to be pretty tough.

- GITAI’s autonomous construction system has already shown it can build a 5-meter tower in a lunar analog setting, and it reached Technology Readiness Level (TRL) 7, meaning it’s among the most advanced lunar construction tech being developed right now.

- GITAI also carried out testing using roughly 7 tons of lunar regolith simulant, basically checking that robotic operations hold up under Moon-like conditions.

- Lunar night lasts about 350 hours, which is around 14 Earth days, and temperatures can drop under 100 Kelvin (-173°C). In certain areas, you can even see readings below -200°F (- 129°C). That kind of cold makes everything harder, especially batteries, electronics, and actually moving the machine around, not just “surviving” it.

- NASA’s Commercial Lunar Payload Services (CLPS) is worth roughly USUSD 2.6 billion, and while the planned Firefly Blue Ghost lunar mission on its own comes in at a contract value of about USUSD 176.7 million, it also includes rover deployments that back Artemis objectives.

- So, the above statistics kind of show that lunar surface robotics is shifting fast into this big-budget, industrial kind of sector.

- With cargo needs moving from the hundreds of kilograms up to tens of thousands, plus multi-billion-dollar government investments, and autonomous systems that are more capable every year, lunar mobility and regolith operations are turning into core technologies for the Moon’s future economy.

Conclusion

Space robotics is kinda rapidly becoming one of the most important enabling technologies in the modern space economy. Strong market growth, rising investment, and increasing deployment across satellite servicing, debris removal, orbital manufacturing, and lunar exploration basically show the sector’s expanding strategic value. Governments still sit as the biggest source of funding, but commercial chances are accelerating, especially as autonomous systems become essential for sustainable space operations.

From multi-billion dollar robotic infrastructure programs to next-generation lunar mobility systems, robotics is reshaping how missions get done beyond Earth. And as orbital activity plus lunar development keep expanding, space robotics will likely play a central part in backing future exploration, infrastructure, and commercialization efforts.

FAQ

It is expected to reach around USD 8.50 billion by 2030.

The sector is forecast to expand at a 9.5% CAGR between 2025 and 2030.

The ADR market is projected to grow to almost USD 2.52 billion by 2032.

According to ESA, there are more than 36,000 trackable debris objects in orbit.

Future Artemis-era logistics concepts anticipate moving as much as 15,000 kilograms of cargo per traverse.